Jürgen Hammer is the InFiNe.lu scholar attending this year’ Strategic Leadership in Inclusive Finance Programme of the Harvard Business School – Accion. From April 17 and for 6 days, Jürgen will be sharing here his experience from Boston and the insights of his participation in the executive programme.

DAY 0 – Before it all starts

DAY 1 – Introduction and 1st case discussion / April 17th

DAY 2 – The Incubents with 4 cases studies / April 18th

DAY 3 – The Disrupters – Disruptive innovation and its opportunities and challenges / April 19th

DAY 4 – Impact Investing – The Investor Perspective / April 20th

DAY 5 – Business and BOP / April 21st

DAY 6 – Leadership and Future Directions / April 22nd

Arriving a day or better two before the beginning of the programme and making a stop in Boston city is really recommended – not only to get over your jet-lag and be fresh for the start, but most of all to live a bit of Boston. AAA quality of life here – a lot of green, the river and sea, and easy to get around. And a lot to see !

I decided to stay in South End, a former run-down and neglected area of town. But in the 1970s, residents organised themselves and filed an application with the City of Boston to make their neighborhood a Landmark District. The project: an innovative and creative renewal cooperation, where professional planners and urban designers worked closely with residents and business owners to help them make their neighborhood better. And the result of this planning and community engagement process is stunning: South End has turned into a beautiful residential area full of impressive Victorian rowhouses and industrial buildings.

Get a bike and move around town, very easy, people very friendly and helpful – and loads of US history on your ways.

Get a bike and move around town, very easy, people very friendly and helpful – and loads of US history on your ways.

With this start, you are in perfect shape and ready for Harvard City – the town of the Harvard Business School.

Located in Northwest of Boston, on both sides of the Charles River, Harvard University really is a town by itself.

It is the US’ oldest institution of higher learning (established in 1636), and in an area of over 85 ha it proposes 11 academic units, residential campuses for over 20.000 students, the Business School, impressive athletic facilities including Harvard Stadium and a lot more. And of course the famous Harvard Library – largest academic and private library system in the world, comprising 79 individual libraries with over 18 million volumes.

Bearing in mind that Harvard’s alumni include among others 8 US Presidents and some 130 Nobel laureates, there is obviously no limit of opportunity to get inspired and to want to learn more!

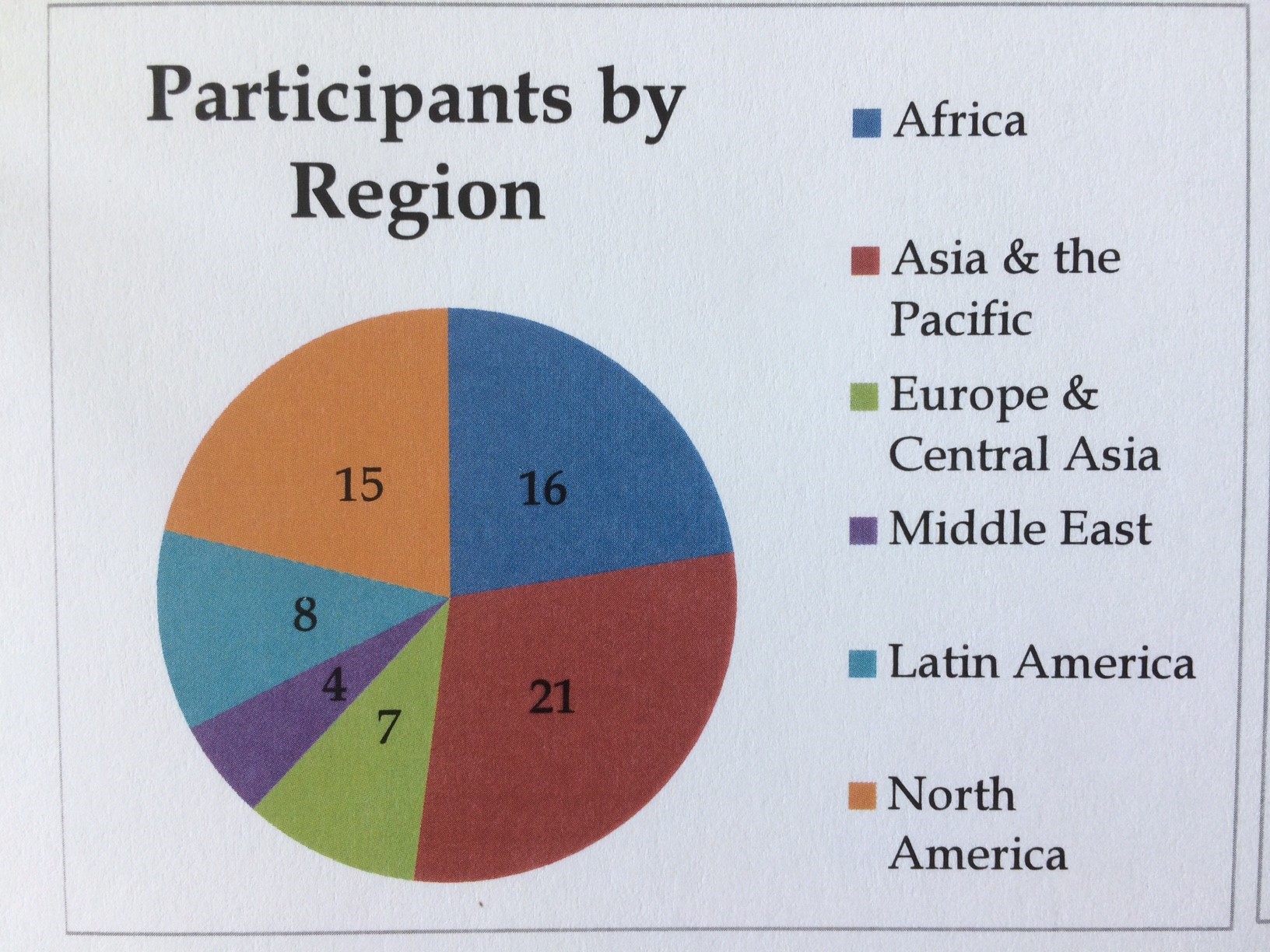

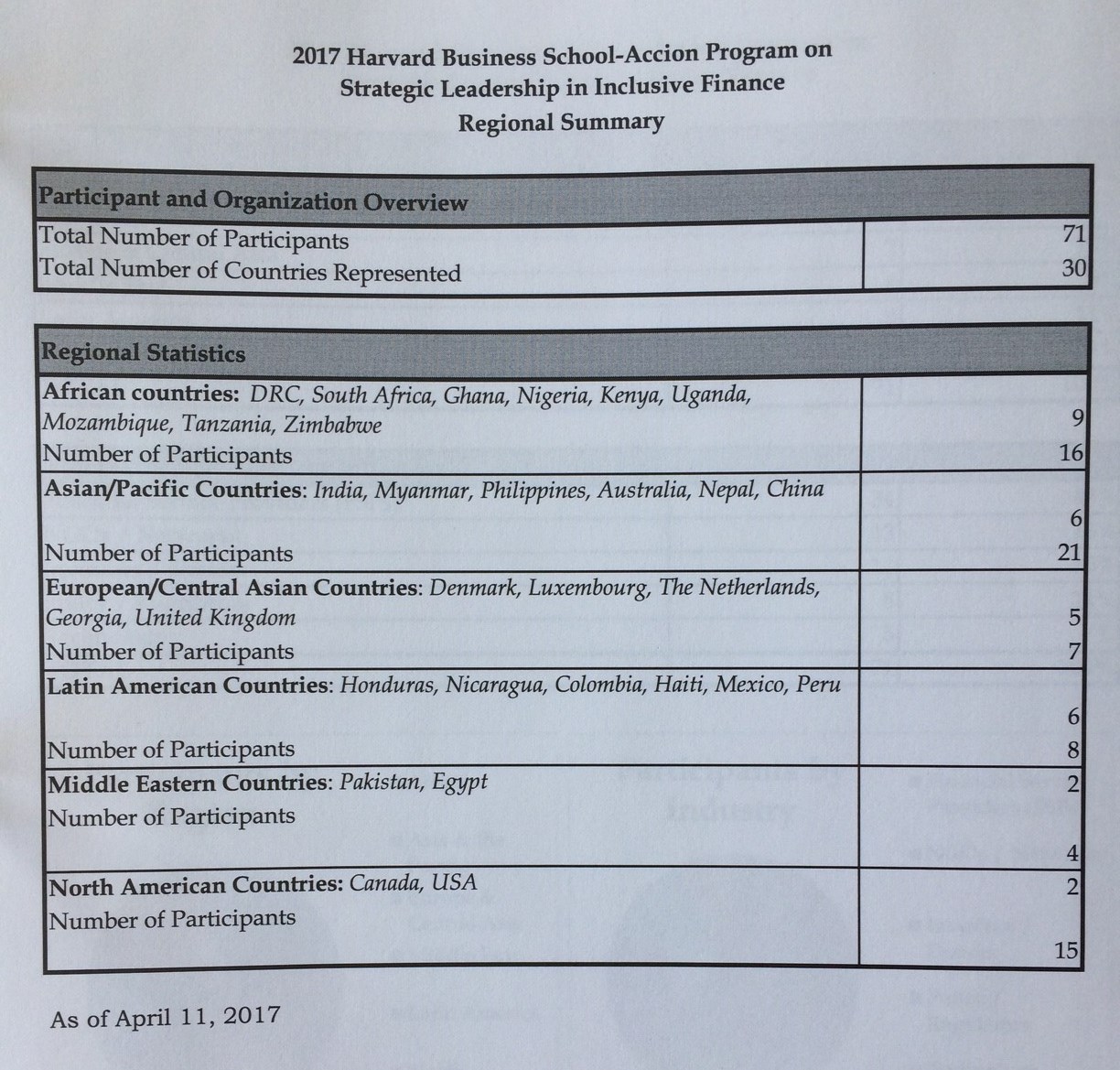

A total of 71 participants from 30 different countries

This first day starts with a general introduction to the program and its specific “HBS methodology”: in the famous HBS “case study” methodology – to the difference of the traditional “teaching by lecture” – learning takes place in the discussions. The 15 cases that will be discussed in the next 6 days (and that all participants had to read before arriving) are not cases of “best practice” but a presentation of reality of situations that allows for diverse interpretations. There is no right answer – it is all about creating valuable frameworks by the combined experience of the participants – in the case of this group an average of 15 years of professional lives…

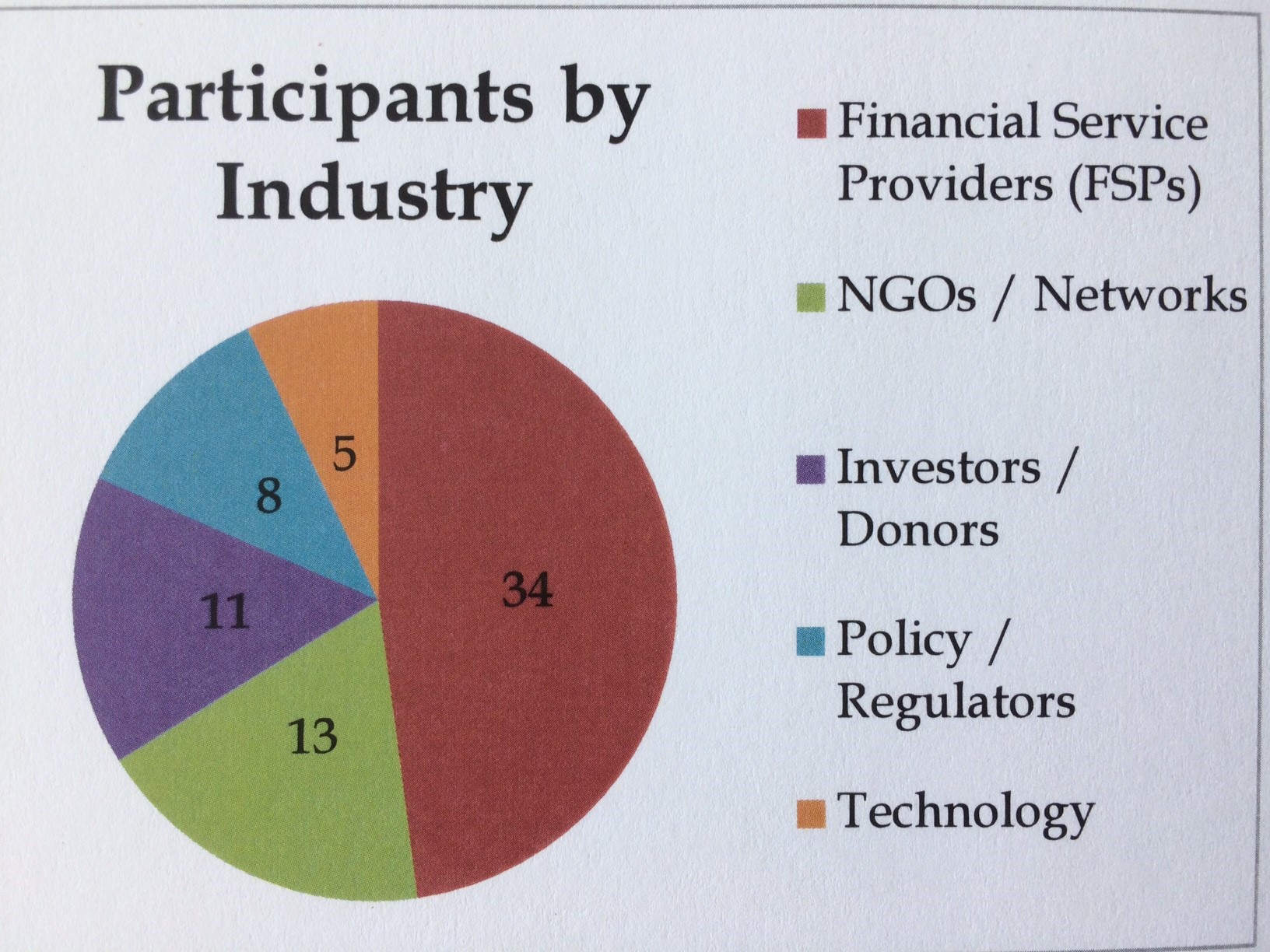

In its 12th year since conception and with over 750 people trained to date, the program continues to adapt to a constantly changing environment of the financial inclusion landscape: 5 representatives from FinTech and 8 from regulators demonstrate the growing importance of new actors and the increasing challenge to adapt regulation to a rapidly changing industry.

The curriculum of the 5 days also reflects the expanding fields of our industry that HBS structures along 6 sections:

Case study on this Mexico-based retailer that expanded across Latin America providing largely credit-based (over 60% of sales) access to basic goods and services at affordable prices to low income populations.

The question discussed was how to classify ELEKTRA within a grid of High/Low commercial value and High/Low social value. Commercial value was not much of a controversy – the group continuously presents positive results – but how to assess the question of Social Value? Within the group no consensus seemed to appear, and opinions varied to the extremes. It became clear that you cannot assess whether a project or a company have social value without a prior clear definition of what this means.

Social Value is additionality + accessibility + impact/scale. ELEKTRA does achieve all these, and can in addition in many aspects be described as a responsible lender. But then what is the difference between a primarily low cost retailer that sells largely on credit and an MFI?

Would the difference be intentionality – the intention of doing good and providing social value? If a business has the intention to provide social value than it needs to define its objectives and measure progress towards achieving this goal.

The wrap up of this first case gives some elements to the initial question: today, retail sales only contribute for about 1/3 to ELEKTRA’s activities. By 2016, credit business, initially only offered to support the sales of the retailer, has become its main business – independent on the need of access to basic goods which was the initial offer of this leading retail chain.

Each day of the week starts at 7h30 with a one-hour meeting of this years’ 9 “Discussion Groups”. Each DG consists of seven or eight participants – formed by HBS prior to the start of the program to include in each group a variety of experiences and sectors represented among all participants.

In addition, to facilitate the interaction, the rooms of the participants of each group form an apartment-like unit in the house, with a living room, large work desk, kitchen and full office facilities. I call it the “inclusive family :-)”.

DGs meet before the daily program starts to discuss the day’s assignments – each participant having previously completed the individual case preparations. DG are characterized by the intense interaction that targets to deepen the participants’ understanding beyond that gained through the individual analysis. In the DG, the cases are discussed and the questions commented – allowing for a better understanding of the case discussions in the full class during the day.

Main benefits of these DG pre-discussions include:

My DG has representatives from the US, Nigeria, DRC, Georgia, Haiti, Pakistan and Ghana – working with MFIs, DFIs, MIVs and networks.

It’s the most intense day with 4 cases that address each a specific topic of the industry landscape:

Cases 2 – 4 were already discussed in last year’s HBS Program and are described on last year’ scholar blog link.

The case describes the development and introduction of a price-linked savings product in South Africa: in 2004, the South African government requested the banking sector to reach out to the roughly 30 million black South Africans who did not use banking services at that time. FNB decided to launch a new savings product, patterned after successful products developed earlier in the UK, the Middle East and Latin America, which offers savers a chance to win a high cash price each month, rather than receiving predictable but unexciting interests.

The class discussions analyzed whether the model of linking regulated financial services with a lottery concept could be considered as justified in order to achieve behavioral change by low income populations, who have an aversion to financial institutions. Is the reputational risk out-weighting the potential benefits of achieving targets of financial inclusion?

The debate did not reach consensus, far from this. In any case, after 3 years, the South African Supreme Court closed the product. 500.000 new clients had been added to bank in the 3 years of existence of this savings product.

But what is a successful inclusion play? Unfortunately, there is not sufficient numerical evidence about how many of these customers were effectively new to banking, nor how many were still a client and had been “included” throughout the following years.

Day 2 ended by a voluntary session (not part of the official program) organised by the CFI, Center for Financial Inclusion at Accion on “How to assess and evaluate financial health”.

Even though both cases building the learning basis of DAY 3 on disruption (or innovation) had already been discussed in last year’s Program (see blog link), the speed and creativity of technological innovation, in particular for data collection, usage and storage, lead to a very different picture from one year to the other.

As introduction and a very lively complement to the pre-reading and early morning Discussion Group analysis, a Senior M-PESA manager and early user of its services who is part of this year’s group shared a very convincing testimony: M-PESA was an immediate success in Kenya because it provided:

It became a huge success, achieving a market share in payments of 85%.

The morning program continued with the discussion of Master Card’s experience and challenges in introducing cash-less transactions in South Africa and Nigeria.

These examples of disruptive innovation in delivery channels led to animated discussions on the definition of “FINANCIAL INCLUSION”? Is FI just ACCESS? ACCESSS and USAGE? And QUALITY?

The views differed widely within such a diverse group of practitioners. Financial Inclusion is first of all an OUTCOME for clients, that allows him to fulfill his needs. Yet targeting financial inclusion brings challenges

As a practical illustration, a presentation followed on DEMONETISATION with the recent example of India’s decision in November 2016 to withdraw from circulation all currency bills of Rs 500 (8 USD) and Rs 1.000 (15 USD). This represented 86% of the currency in circulation. The objectives of this surprise measure, besides tackling corruption and terrorism financing, was to push for increased digitalisation – hoping to increase financial inclusion in the country. 5 months later, about 75% of the currency taken out previously has been put back into circulation.

Nevertheless, the experience demonstrated that a major shift is taking place, that will affect not only microfinance but the entire finance sector: while in the developed markets, we moved progressively from BRANCH BANKING > BANKCARDS > INTERNET > MOBILE BANKING, countries like India demonstrate that the move for the large majority of the developing markets will simply skip the BANKCARD and INTERNET phase and move directly to MOBILE. The implication for the traditional (retail) banking sector and microfinance may well reveal enormous: competition for banks and MFIs is no longer coming from other banks or from other MFIs, but a full set of totally new companies.

And most probably much further: Fingerprint ID and DBI (DIGITAL BIOMETRIC IDENDITY) are even cutting the MOBILE BANKING step out of this evolution. Even if DIGITALISATION never had the objective of Financial Inclusion and can be considered as a spill-over effect, it will deeply affect our industry. And whether we like it and welcome it, or not – this is already there.

Now why is this so important?

Many participants in the group warned that the impact on small or mid-sized banks and MFIs will be substantial. Organisations that don’t have the resources to adapt and introduce new technologies risk to be out of business once big players have access to their customer data.

The solution is among all to better engage with customers to create trust beyond the technological solutions.

See also link from HBS 2016

The IPO of this Chinese P2P platform led to an intense, and at moments emotional exchange and confrontation of ideas between the diversity of participants: the real value of the company is its credit analysis methodology, i.e. its data-based credit engine using the information of the internet. Once it receives permission from a potential lender to access all personal data, credit capacity can be assessed in no time and algorithms determine the credit capacity = the probability of success (repayment) or failure (default).

But who is the owner of the digital footprint that every one of use today produces? What should the role of regulators be in this space?

HBS organised this informal exchange between the ACCION executive group and HBS MBA students. An interesting opportunity for both sides to discuss questions and exchange with future potential economic leaders on preoccupations, ideas and trends in career planning, as well as issues of responsibility and inclusion in the financial sectors.

Second half of the program already …. And for the analysis of the investor perspective we leave the field of microfinance and financial inclusion for the larger sector of impact investments. Three different philosophies and three different regions (India, Kenya, Brazil) provide for a large spectrum of topics, challenges and approaches.

This day also finally introduces the concept of social performance and impact evaluation – the various methodologies and initiatives, their strengths and their limitations.

ACUMEN is considering 2 investment options: Ecotact, a for-profit venture that aims at providing clean and accessible toilet and shower facilities in and around Narobi and Merian, a group of private health clinics planning to establish a chain of low-cost, high quality outpatient clinics across Kenya.

An assessment matrix based on mission, financial sustainability, potential for scale, social impact and management capacity provides the framework to evaluate, compare and prioritize the investment options. The criteria of social impact leads us to discuss different methodologies for impact evaluation such as BACO (Best Available Charitable Option), RCTs and ACUMEN’s intern Lean Data initiative. A lively debate follows on the need for standardized metrics or not, the pros and cons of creating ratios for impact evaluation like those we use in financial analysis, and the weakness of having methodologies driven mainly by investors and not enough by investees. The large variety of views and expectations in the class shows how far away the impact investment market still is from any kind of consensus on these issues…

The example of Brazil’s first impact fund VOX Capital provides the material for analysing how to build an impact investment organisation, and in particular how to get all stakeholders aligned and involved in a shared impact mission.

Different types of investor profiles request different approaches: family offices and HNIs, DIFs, corporates, retail investors and institutional investors such as pension funds or insurance companies.

The discussion then covered the tasks and responsibilities of an investment manager: raising funds, originating investees and developing a pipeline, develop an impact management capacity, defining an implementing focus and mission and – in particular for a first-goer – developing an ecosystem.

At the moment of the case, VOX was about to launch Fund II, an opportunity to apply learnings from the first project. The experience of Fund II revealed the changes coming with the arrival of “the Millenials”. This generation, generally considered to be born between the early 1980s up to the early 2000s, often goes beyond the traditional 2-dimensional investment-vs-philanthropy approach, creating a 3rd option of responsible economic behavior where impact and return are no more considered as contradictory.

The example of Omidyar Network, created by eBay founder Pierre Omidyar and his wife Pam, rounded up this rich round of cases with an innovative approach – a hybrid organization. ON is a limited liability company and a private foundation side by side, united by a single criterion: social impact.

Main issues revealed by the study of Omidyar:

Would we bring this company to the ON Investment Committee? And if yes, should ON decide to support Anudip by grants through the NFP arm? Or the impact investment arm? Or both?

Evening Session by SMART Campaign on the MODEL LAW FOR FINANCIAL CONSUMER PROTECTION

Digital financial services, agent banking, MNOs (Mobile network operators) represent a huge challenge to existing frameworks of consumer protection, client identification (KYC) and globally supervision and regulation of FSP (Financial Service Providers).

SMART and CFI organised this session to discuss with regulators about challenges of regulation and supervision in this rapidly and profoundly changing financial services environment.

Through project Shakti, starting in 2000, the multinational Unilever managed to build on the existing structure of SHGs in rural India to develop a distribution network for its mass consumer products – detergents, personal products and health care, beverages and some food – to the villages and rural areas of India, about 700 million potential customers.

How important is intentionality to the assessment of social value? Was it Unilever’s intention to empower women from the communities by promoting them to become Shakti entrepreneurs? Or was it health and hygiene education to the BOP? Or was it primarily a marketing and sales project?

As a large, multinational capitalistic company, it seems that women really were a means for Unilever to reaching the targeted 500.000 small villages and creating future consumers of its products. Does the intention matter if impact is achieved?

Reflecting the diversity of our group, opinions and analysis diverged largely. But the case helped to raise awareness on the issues of evaluation. What matters needs to be measured, and if it is not measured it will eventually not matter.

In the case of Unilever (in the absence of data on what change did the women’s involvement with Skakti bring to their lives in the long-term), the lack of criteria and data do not allow for a reasonable judgment of the achievement of social value.

Responding to a disfunctionning public health system by developing a network of discount and generic drugs and medical services has allowed FS to grow into a huge pan-Latin-American venture. FS provides a successful example on how to navigate through changing legislation and competitive environments and scale strategies such as franchising.

Here again – is business efficiency and pursuit of financial return objectives contradictory with providing real value to the people of Mexico and many neighboring countries?

Mohammed Yunus’ call for disruptive change and a totally new business model – his concept of Social Businesses – as always provides for passionate and contradictory debates. Is it really possible to create a “third dimension of business”, between philanthropy and commercial focusing on return? How realistic is his approach.

This introduces again the need for client centricity – and the importance to carefully assess cultural fundamentals at all levels of the value chain.

Why has DG still not achieved this sustainability, nor scaled towards its initial expectations? By focusing on the client, perhaps dairy products were not the most adapted way to address the challenges of child malnutrition.

In this 3rd round of group work on identifying the major challenges, proposals were presented on the 6 most important challenges identified by the various groups:

A successful of cross-subsidization has led Aravind to become a model in India and international. A debate accompanied this case about the importance of passion and spirituality?

In its 40 years of age, microfinance has started from a passion and commitment-driven experiment to an industry that has matured and entered into the global financial markets. Funding is no longer the main constraint. Today, approximately 150 million active clients have access to a MF loan, a total of 50-60 bn USD. But total demand may represent over 600 million families worldwide – and 300 bn USD. How can these remaining 75% or people be reached? In the current model, deep customer knowledge is achieved through a labor and cost intensive process. As a result, the growth of the industry as slowed in recent years, despite the potential and needs at the BOP.

For Prof Chu, the 40 old model of microfinance is ripe for disruption, with 3 mega trends that have already started to modify the world, as they allow for an exponential expansion in capabilities. They will help to decrease costs drastically – it is all about DATA!

• ability to PRODUCE gigantic volumes of data through machine intelligence (DFS)

• ability to DISSEMINATE data through internet

• ability to remotely receive, use and send data.

Under these trends, every key factor behind microfinance leadership as of today is under challenge.